Short-run equilibrium in perfect competition

Firm

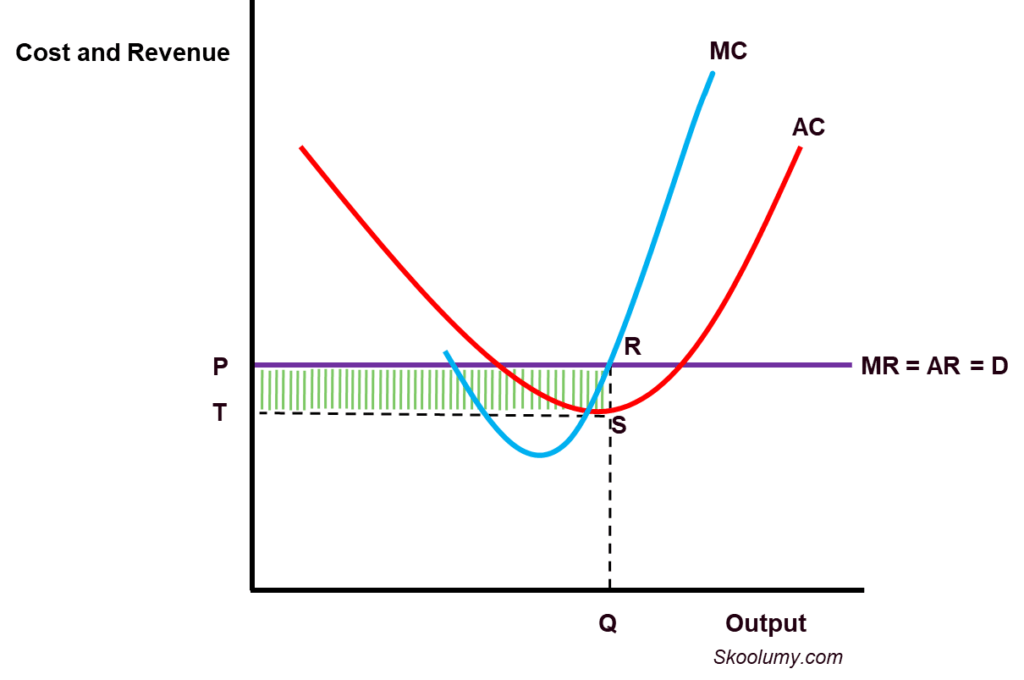

The firm produces at the output level where Marginal Revenue(MR) and Marginal Cost(MC) are equal. This is the profit maximising output since they are profit maximisers. In addition, the Average Cost (AC) curve is below the Average Revenue (AR) curve, thereby generating abnormal profit in the short-run. Abnormal profit, also known as supernormal profit, is the profit above the minimum profit required for a firm to continue operating in the market. The abnormal profit is represented by rectangle PRST in Figure 1 below.

Figure 1: Short-run abnormal profit in perfect competition

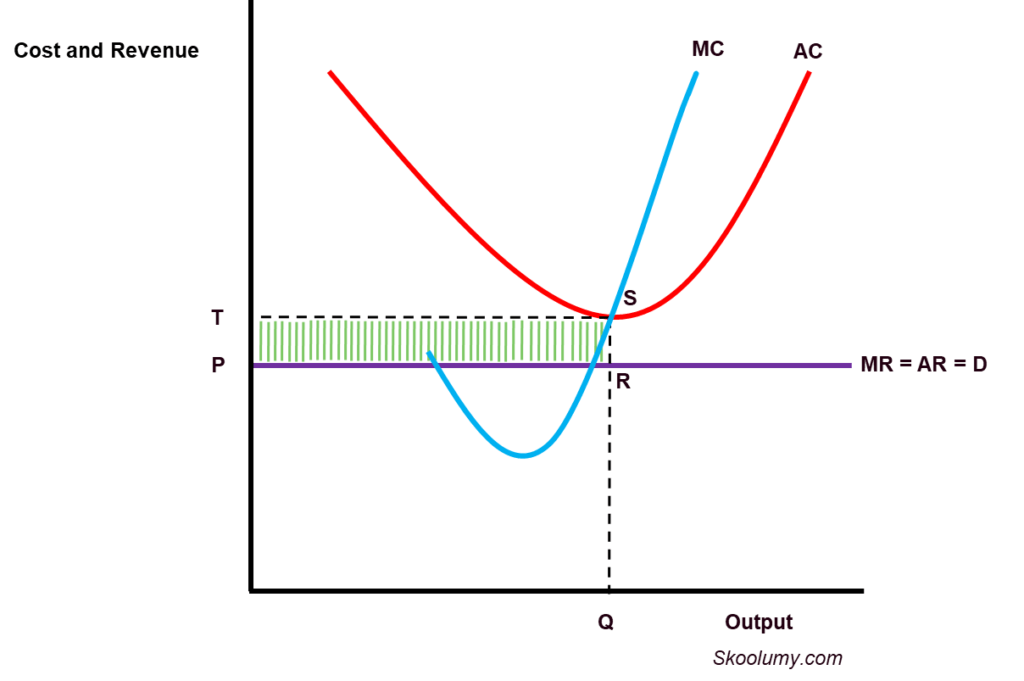

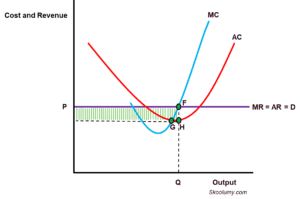

However, the firm can make a loss in the short run instead of abnormal profit. In this case, AC exceeds the AR resulting in a loss (rectangle TSRP in Figure 2).

Figure 2: Short-run loss in perfect competition

Industry

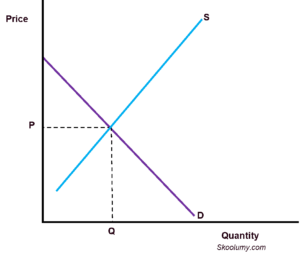

The industry, as a whole, attains equilibrium when industry market demand is equal to the market supply (Figure 3 below). The market demand is the sum of the demand of all the consumers while market supply is the sum of all supplies. Each firm cannot alter output to the extent that it will affect the market supply because its market share is insignificant. Therefore, the supply curve slopes upward. Also, no buyer can influence demand as there are many of them, making the demand curve maintain its downward-sloping nature.

Figure 3: Industry short-run equilibrium in perfect competition

Long-run equilibrium in perfect competition

Firm

In the long run, normal profit is made as Average Cost(AC) and Average Revenue(AR) are equal (Figure 4 below). Normal profit is the least possible amount of profit that a firm has to make to continue supplying its resources in the market. The existence of abnormal profit in the short-run will attract more firms to the industry, thereby eradicating abnormal profit in the long-run.

Figure 4: Long-run normal profit in perfect competition

Industry

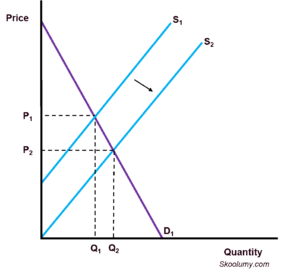

As more firms join the market in the long run, the market supply increases lowering the market price. The total output in the industry increases while the price reduces in the long-run (Figure 4 below).

Figure 4: Industry long-run equilibrium in perfect competition

Efficiency of firms in perfect competition

There are two types of efficiency possible in this type of market structure, namely productive and allocative efficiency. The firms cannot attain dynamic efficiency in this type of market because it is made up of many small firms that cannot afford to invest in the required technology and research and development that assures innovation. There is a need for a lot of abnormal profit which is short-lived in this market since it occurs only in the short-run. The absence of barriers means there will be more entrants into the market in the long-run and abnormal profit will fizzle out.

Efficiency in the short-run

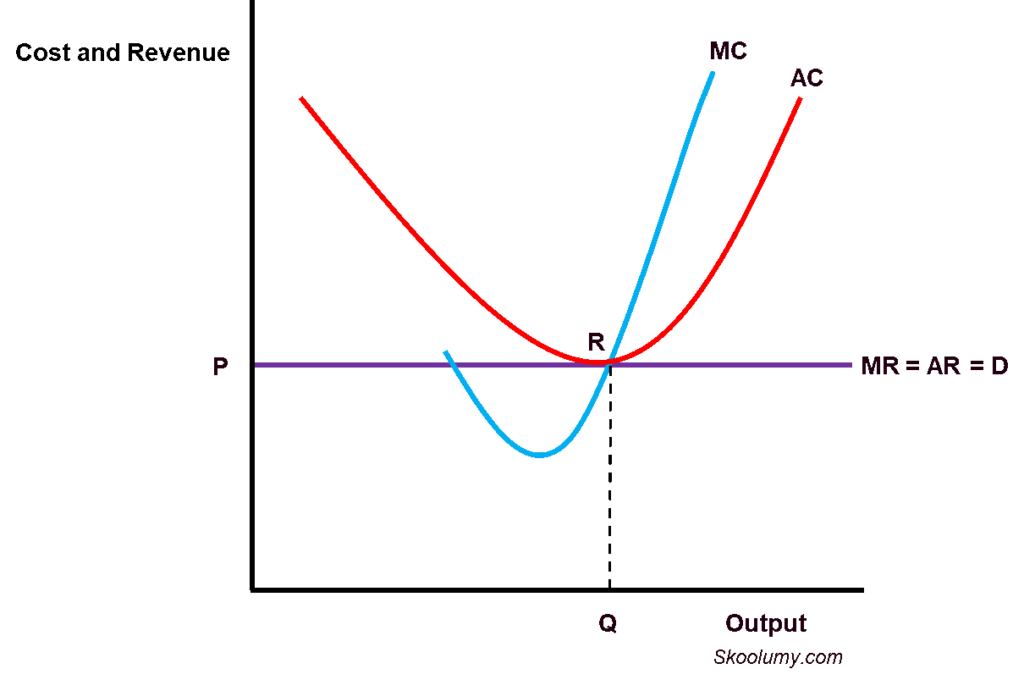

In the short-run, the business will achieve allocative efficiency because the price and marginal cost are equal (P=MC) at the profit-maximising output level Q. The profit-maximising output or equilibrium occurs where marginal revenue and marginal cost are equal. In Figure 5 below, point F, where P and MC intersect corresponds to Q, the short-run equilibrium output of a perfectly competitive firm.

Figure 5: Efficiency in perfect competition in the short-run

However, it is impossible to be productively efficient in the short-run because the firm is not producing at the lowest cost possible, i.e. lowest point on the average cost curve (point G in Figure 5 above). Point H, which corresponds to Q, the equilibrium output level, is not the lowest point on the average cost curve.

Efficiency in the long-run

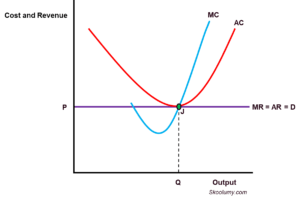

The firm will achieve both productive and allocative efficiency in the long run. The firm will be productively efficient since it is producing at an output level corresponding to the lowest point on the average cost curve (J in Figure 6 above). Also, it achieves allocative efficiency because the output Q can be obtained from Point J where the price and marginal cost curve intersect.

Figure 6: Efficiency in perfect competition in the long-run