Loanable Funds Theory of Interest

Loanable Funds Theory of Interest was proposed by Knut Wicksell, a Swedish economist. It is also known as the Neoclassical Theory of Interest. It is more realistic than the Classical theory because it considers bank credit as an integral part of the money supply. It also considers money as an important factor affecting the determination of interest rate.

According to this theory, the determinants of interest rate are the demand for and supply of loanable funds. Loanable fund is money to be given out as loans or credits. The cost of a loan to the borrower is, therefore, the interest rate.

Economic agents demand for loanable funds for consumption, investment and hoarding purposes. Households normally require loans for consumption while firms obtain credit facilities for the purchase of capital goods. The government borrows when it has a budget deficit, i.e. expected revenue is less than the proposed expenditure. The keeping of idle cash balance is known as hoarding. The demand for loanable funds curve is downward-sloping meaning borrowing will increase as the interest rate falls.

The supply of loanable funds is from savings (personal and corporate) bank credit and dishoarding. Higher interest rate increases savings, dishoarding and bank loans. The supply of loanable funds is represented by an upward-sloping curve because more loans would be given out if the interest rate is high.

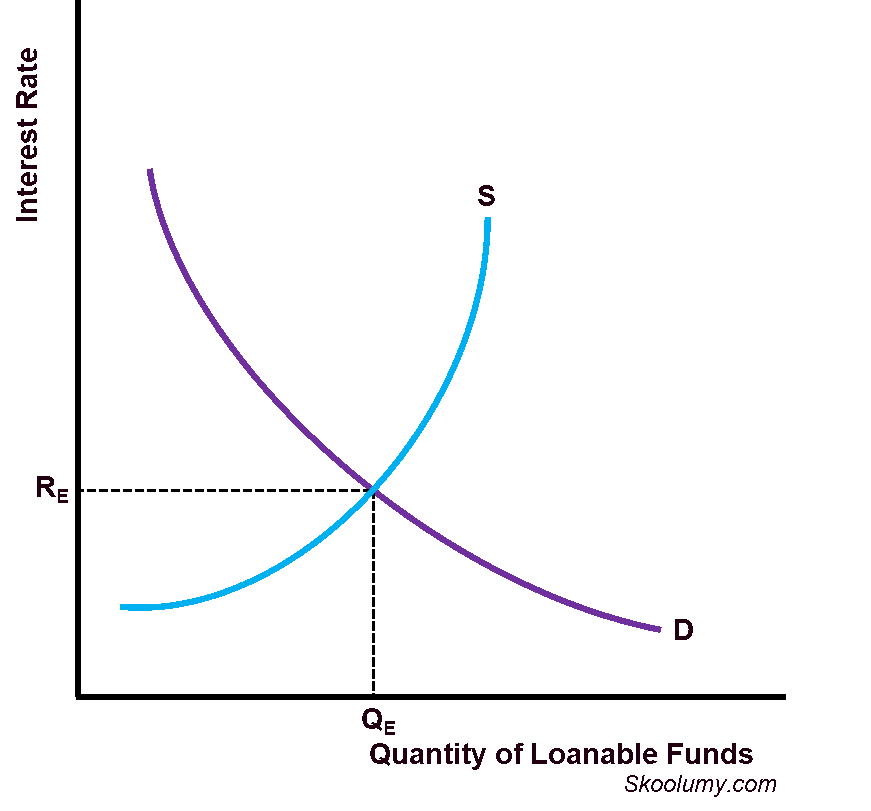

Figure 3: Demand and supply of loanable funds

In Figure 3 above, the interest rate of RE is produced by the intersection of demand for and supply of loanable funds.

In Figure 3 above, the interest rate of RE is produced by the intersection of demand for and supply of loanable funds.

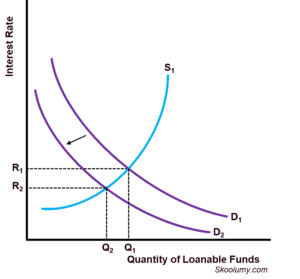

Figure 4: A decrease in demand for loanable funds

A decrease in demand for loanable funds will shift the demand for loanable funds from D1 to D2, thereby reducing the interest rate from R1 to R2 (Figure 4 above).

The Liquidity Preference Theory of Interest (Keynesian Theory)

According to the Liquidity Preference Theory, interest rate is determined by the intersection of the demand for money and the supply of money. It is the rate at which the desire to hold liquid assets is equal to the volume of money in circulation. Demand for money is the preference to hold liquid assets, such as cash, as against holding other less liquid assets, such as bonds. The demand for money curve slopes downward from left to right; that is to say, demand for money decreases as interest rate increases. This is because people will keep less cash and invest in assets like bonds when the interest rate is high.

The supply of money is the total amount of money circulating in an economy. The supply of money is assumed to be fixed by the authority; therefore, it is a perfectly inelastic or vertical line.

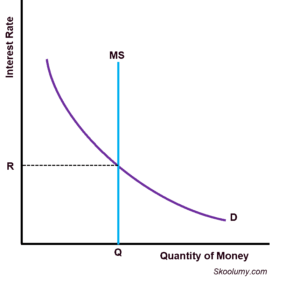

In Figure 5 below, R is the interest rate at which demand for money (or liquidity preference) is equal to the money supply. The money supply exceeds the demand for money at any interest rate above the equilibrium interest rate (R). This will drive the interest rate down to R. Also, the demand for money surpasses the money supply at any interest rate below R; this means there is a shortage or scarcity of money. Therefore, the interest rate will increase until the equilibrium is restored.

Figure 5: Liquidity preference theory of interest

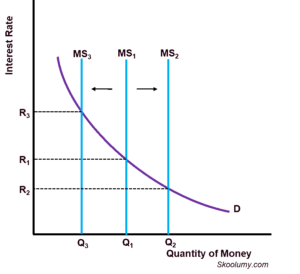

The government or central bank can increase the amount of money in circulation for the interest rate to decrease or reduce the amount of money in circulation for the interest rate to rise. An increase in money supply from MS1 to MS2 reduces the interest rate from R1 to R2. The interest rate rises from R1 to R3 when the money supply is decreased from MS1 to MS3 (Figure 6 below).

Figure 6: Effect of changes in money supply on interest rate