Errors that do not affect the agreement of the trial balance

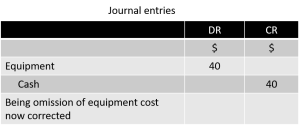

Correcting the error of omission

The debit and credit entries have been completely omitted from the accounts. To correct this kind of error, the correct entries are made. For example, a purchase of equipment for cash of $40 has not been recorded in the accounts. The correct entry is to debit the equipment account and credit the cash account.

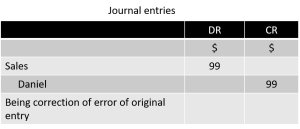

Correcting the error of original entry

An incorrect amount has been posted to both the debit and credit sides of the relevant accounts. For example, a credit sale of $102 to Daniel has been entered as $201 on both debit and credit sides of the correct accounts. Daniel’s account has been debited, while the sales account has been credited with $201.The entries have been overstated by $99 $201-$102). Reduce the debit entry by posting the difference to the credit side of Daniel’s account. The sales account is debited with $99.

Correcting the complete reversal of entries

This error involves reversing the double-entry principle; the account to be debited is credited while the account to be credited is debited with the correct amount. For example, a rent of $100 paid by cheque has been debited to the bank account and credited to the rent account. The normal procedure is to debit the rent account with $100 and credit the bank account with $100. Double the amount to $200 and enter it on the correct side of the accounts to correct this error. The bank account is credited with $200. The first $100 will cancel out the error; the remaining $100 is the correct amount to be entered on the credit side of the bank account. Likewise rent account is debited with $200 to leave a balance of $100 on the debit side after cancelling the initial error.

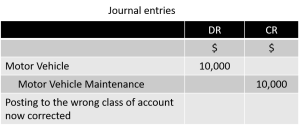

Correcting the error of principle

The wrong type of account is used to observe double-entry. For example, the purchase of a motor vehicle for $10,000 has been debited to the motor vehicle maintenance account. Motor vehicle is an asset while motor vehicle maintenance is an expense. The error is eliminated in the motor vehicle maintenance account by crediting it. The correct entry is then made by debiting the motor vehicle account with $10,000.

Correcting the error of commission

The wrong account is used, but it belongs to the same class of accounts as the correct account. For example, the sale of goods for $500 to Matt is debited to Matthew’s account. Eliminate the entry in Matthew’s account by crediting it. Then, the correct entry is made on the debit side of Matt’s account, the appropriate account.

Correcting compensating error

An error in one account cancels out the error in another account. Assuming the purchases account was debited with $150 instead of $50. At the same time, the sales account was credited with $800 instead of $700. Obviously, both the debit and credit sides have been overstated by $100. The correction is to reduce both sides by $100. To reduce the amount in the purchases account, $100 is credited to the account. Debiting the sales account with $100 will eliminate the error in that account.