What is maximum price?

A maximum price is the highest price that can be charged for a product. It has to be fixed below the equilibrium price to be effective. This is usually used by the government to make a product affordable because the market price is too high. A maximum price is a price control used for essential products such as staple foodstuffs and rent. It is also known as a price ceiling as consumers cannot be asked to pay higher than it buy they can be charged a lower price. It creates a problem of shortage or excess demand as the quantity demanded increases at the lower price while the quantity supplied decreases. This often leads to queues or the adoption of waiting lists by businesses. In the long run, the suppliers may be discouraged from offering the product unless the government does something about it. In addition, it may be difficult to attract new investments. For instance, the use of rent control will eventually make landlords use their houses for other purposes apart from renting them out.

Figure 1: Maximum price

The quantity demanded Qd exceeds the quantity supplied Qs (shortage) due to the imposition of a maximum price below the equilibrium price P. The quantity traded in the market is Qs as the consumers cannot buy more than the quantity Qs offered by the suppliers. This means that not every consumer can obtain the good. The government may have to ration the goods by distributing a fixed amount to each individual to ensure everyone has access to the goods. If the government does not intervene by rationing, firms will give preference to their loyal customers, thereby preventing others from having access to the good. A black market may develop where the goods are sold above the maximum price. Because of the scarcity, some consumers may be willing to pay more than the original equilibrium price P.

If a buffer stock scheme is in place, the government may release some goods from the buffer stock. It may also intervene through direct provision, granting subsidies or tax incentives.

Effect of maximum price on welfare

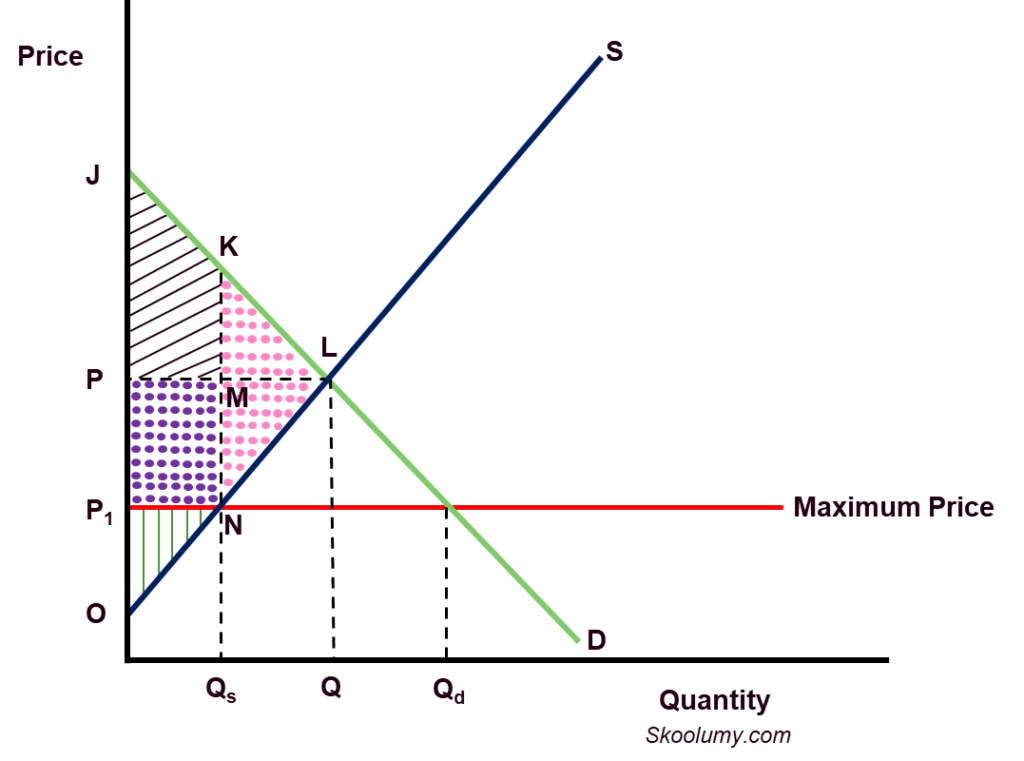

Figure 2: Maximum price and welfare

Maximum price and consumers’ welfare

The consumers pay the maximum price P1 which is lower than the equilibrium price P. The initial consumer surplus is the area of triangle JPL. The new consumer surplus is the area of trapezium JP1KN which is bigger than the initial consumer surplus. This means that the welfare of the consumers has improved. KML, part of the initial consumer surplus, is lost while PP1MN, part of the initial producer surplus is gained by the consumers as part of their new surplus.

Maximum price and producers’ welfare

There is a loss of producer surplus and welfare as a result of the introduction of a maximum price. The initial producer surplus is shown by the area of the triangle POL. But the new producer surplus is P1ON which is smaller than the initial producer surplus. The lost surplus of the producers is the area of the trapezium PP1LN.

Maximum price and economic welfare

The overall loss to the economy is represented by the triangle KNL. This is also called deadweight loss. The quantity traded Qs is less than the optimum quantity, i.e., the equilibrium quantity Q. The desired production or consumption does not take place, resulting in welfare loss to the society.

What is minimum price?

A minimum price is the lowest price that can be charged for a product. The government fixes this in order to intervene in the market when it thinks the equilibrium or market price is too low. The minimum price has to be set above the equilibrium price in order to be effective. It is also called a price floor as the price is not allowed to fall below it, but it can rise above it. For example, the government may believe that the price of alcohol is too low because it has negative effects on third parties. And it will fix the minimum price for it. This means that it cannot be sold below the fixed price, but it can be sold above it. A minimum price can also be used to protect the producers so that they get a high price for their products, e.g., farmers.

Figure 3: Minimum price

Because it is above the market price, the quantity demanded will decrease (the Law of Demand) while the quantity supplied will increase (the Law of Supply). Therefore, the quantity supplied will outstrip the quantity demanded and produce a surplus (excess supply). In Figure 1 above, the quantity demanded is Qd which is less than the quantity supplied Qs, resulting in a surplus of from Qd to Qs. The quantity traded in the market is Qd as producers cannot sell more than the quantity consumers demand. Unless the government buys the excess supplied or restricts supply by setting production quotas, firms would want to clear their excess stocks by illegally selling below the stipulated price. This will defeat the purpose of the price control.

One other drawback of this policy is that firms would not strive to achieve efficiency because they are protected by the high price fixed by the government. They would not reduce their costs (productive inefficiency) or produce alternative products that consumers want more (allocative inefficiency).

Effect of minimum price on welfare

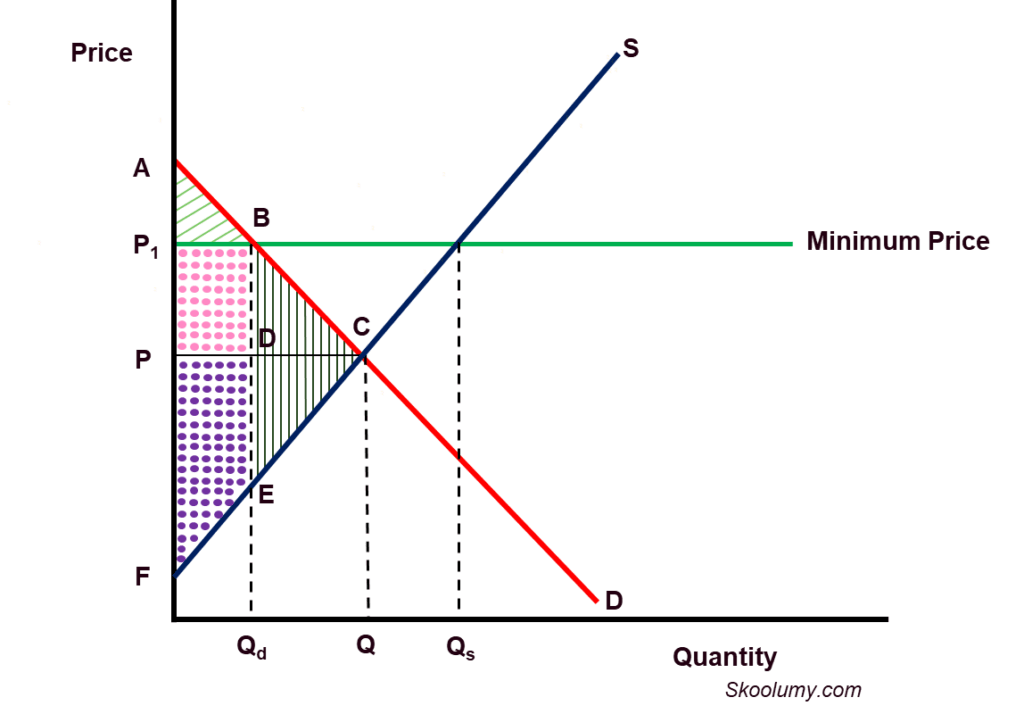

Figure 2: Minimum price and welfare

Minimum price and consumers’ welfare

The price paid by the consumer P1 (minimum price) is higher than the equilibrium price P and the quantity purchased Qd is less than the equilibrium quantity Q. Thus, the welfare of the consumer has worsened. This can be buttressed by a decline in consumer surplus which is a measure of the welfare of the consumers. The initial consumer surplus at equilibrium is the area of triangle APC; the new consumer surplus after the minimum price P1 was fixed is the area of triangle AP1B. The consumer surplus (welfare) lost is the area of the trapezium P1BPC.

Minimum price and producers’ welfare

The producer receives price P1 which is higher than the equilibrium price P. The initial producer surplus at equilibrium is the area of the triangle PFC. The consumer surplus at the minimum price is the area of the trapezium P1BFE. The producer benefits by obtaining a greater producer surplus (welfare).

Minimum price and economic welfare

The economic welfare arising from the imposition of a minimum price is the addition of consumer surplus and producer surplus. The overall effect on the society is a welfare loss represented by the triangle BEC. The consumer surplus lost area is represented by the trapezium P1BPC. The producer surplus lost triangle DCE but gained part of the lost consumer surplus ( rectangle P1BPD). The economic welfare loss (triangle BEC) is also referred to as deadweight loss. The quantity traded Qd is below the equilibrium quantity Q. It is at equilibrium that welfare is maximised and inefficiency is eliminated. In other words, both consumer surplus and producer surplus are at the highest level when there is equilibrium.