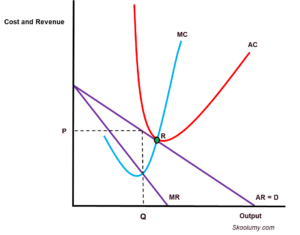

Short-run equilibrium in monopolistic competition

The firm produces at the output level where marginal revenue (MR) and marginal cost (MC) are equal. The average cost (AC) is below the average revenue (AR) leading to an abnormal profit in the short run. In Figure 1 below, the output Q occurs where MR is equal to MC as a profit maximiser. The rectangle PRST represents the abnormal profit made as the AR is greater than the AC.

Figure 1: Short-run equilibrium of a monopolistic competitive firm

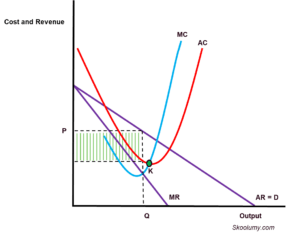

Long-run equilibrium in monopolistic competition

In the long run, however, normal profit is made as AC and AR are equal (Figure 2 below). The relative ease of entry makes the short-run abnormal profit disappear in the long-run.

Figure 2: Long-run equilibrium of a monopolistic competitive firm

Efficiency in monopolistic competition

Monopolistic competition, an imperfect market structure, does not attain any type of efficiency. Productive and allocative efficiency do not exist in both the short- and long-run. In addition, dynamic efficiency cannot be attained since the short-run abnormal profit can be competed away in the long-run; the low barriers in a monopolistic competitive market mean that the firms cannot make an abnormal profit in the long-run to embark on innovation, research and development which are required to achieve dynamic efficiency.

Efficiency in the short-run

A firm in a monopolistic competitive market does not attain productive and allocative efficiency in both the short-run. It does not produce at the output level where the average cost is at the lowest,i.e. there is no productive efficiency. In Figure 3 below, the equilibrium output Q is not determined from the lowest point on the average cost curve (point K). Also, there is no allocative efficiency because the price and marginal cost curve do not intersect or meet at the profit-maximising output Q in the short-run (Figure 3 below).

Figure 3: Efficiency in monopolistic competition in the short-run

Efficiency in the long-run

In the long-run, the firm does not produce at Point R where productive efficiency is achieved (Figure 4 below). The price and marginal cost curve do not intersect at a point that can be traced to Q, the equilibrium output level, thereby making allocative efficiency impossible in this type of market efficiency.

Figure 4: Efficiency in monopolistic competition in the long-run